Master Cash Flow Management for Financial Freedom

FINANCIAL INDEPENDENCE

Trixy

8/1/20254 min read

Building on your balance sheet foundation, it's time to tune the pulse of your finances.

Why Monthly Cash Flow Is Non-Negotiable

Your cash flow is the heartbeat of your financial life. A strong, steady pulse funds emergency buffers, career pivots and accelerated wealth building. A weak or erratic pulse—more money out than in—puts every goal at risk. Monitor it, or drift.

The Midlife Reality Check

At 40-50 you juggle large mortgages, school or university fees for your children, ageing parents and compressed timelines. You cannot wait decades. Cash-flow clarity lets you:

Cover essentials without debt anxiety

Stockpile a 6-12-month emergency fund before you resign or retrain

Redirect surplus towards high-yield assets, not lifestyle creep

The Age-Adjusted Framework: More Aggressive, Less Time

Forget the usual 50/30/20 advice. You need acceleration.

Ages 40-55: The Sprint Phase (50/30/20)

50% essentials (housing, food, transport, insurance)

30% wealth-building (investments, pension top-ups, debt prepayment)

20% lifestyle (restaurants, hobbies, holidays)

Ages 55-65: The Final Push (45/35/20)

45% essentials (tightened but realistic)

35% wealth-building (maximum acceleration before retirement)

20% lifestyle (maintained for quality of life)

Ages 60-65: Catch-Up Mode (40/40/20)

Starting late or behind targets? Go harder:

40% essentials (bare bones efficiency)

40% wealth-building (emergency wealth-building mode)

20% lifestyle (non-negotiable minimum)

Tight? Absolutely. Necessary? Yes, if you want financial freedom before 70.

Three-Step Cash-Flow Audit

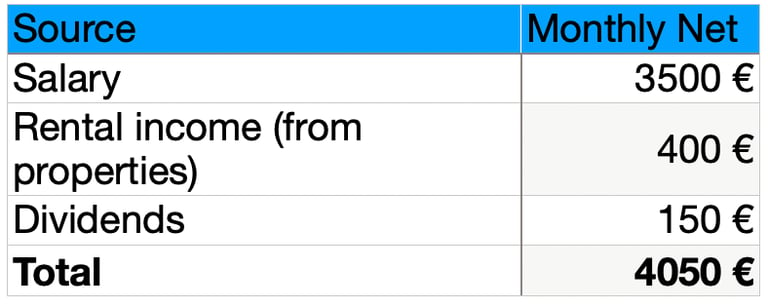

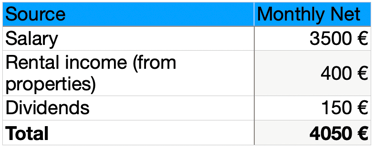

1. Track Every Euro In

List all after-tax income streams: salary, side gigs, rental income, dividends.

Example:

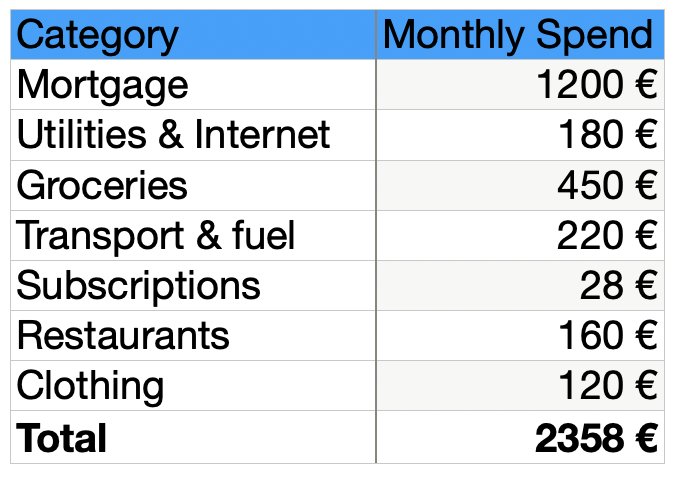

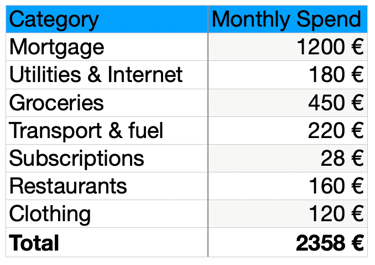

2. Track Every Euro Out

Capture everything—standing orders, card taps, cash.

Example:

3. Calculate the Cash Flow

Monthly Cash Flow = Income − Expenses

Example:

4.050 € − 2.358 € = 1.692 € surplus.

For Ages 40-55 (30% wealth-building target = 1.215 €):

800 € to index funds/pension

415 € extra mortgage principal

477 € lifestyle buffer

For Ages 55+ (35-40% wealth-building target = 1.420-1.620 €):

1.000 € to index funds/pension

420 € extra mortgage principal

200 € emergency fund top-up

72-272 € lifestyle

Zero idle money: every euro has a purpose.

Common Midlife Leaks to Plug

The Big Four Wealth Killers

Lifestyle inflation: Your 20% raise becomes 40% spending increase

Adult child syndrome: Supporting 25-year-olds indefinitely

Idle cash hoarding: Emergency fund beyond 12 months earning 0.1%

Subscription creep: €200+ monthly on forgotten services

Age-Specific Leak Patterns

Ages 40-50: Career celebration spending (new car, house extension)

Ages 50-60: Pre-retirement panic buying (courses, equipment, holidays)

Ages 60-65: "Final years" splurge mentality before belt-tightening

Plug them all. You have no margin for error.

Make It a Habit: The Monthly 30-Minute Audit

Week 1 of each month:

Update income and expense columns

Calculate surplus against age-appropriate targets

Redirect excess the same day (zero delay tolerance)

Identify and plug new leaks immediately

Consistency beats perfection. Miss a month, lose momentum. Stay disciplined.

You can do your calculations on paper if that's your thing, or hop onto Excel for some digital number-crunching. Alternatively, find a cozy spot and get comfortable with your own financial tracking.

And, as an added bonus, I've got a free Google Sheets template just waiting to be customized by you! Download this super helpful document, and start tracking your finances like a pro - all without breaking the bank (because it's totally free, of course)!

Linking Back to Your Balance Sheet

Your balance sheet (covered in "Balance Sheet for Financial Independence: The Non-Negotiable First Step") shows net worth at a point in time. Cash flow shows the velocity of money entering and leaving. Together they reveal:

Whether you are asset-rich but cash-strapped (common among high-equity homeowners)

If liabilities—consumer credit, car loans—are choking future investment capacity

How quickly you can reach a 12-month runway and pivot careers without panic

The Reality Check: Can You Handle This?

If you're 45 and saving 15%: You are financially sleepwalking. Wake up.

If you're 55 and saving 20%: Better, but still behind. Accelerate now.

If you're 60 and saving 25%: Cutting it close. Consider the 40/40/20 emergency protocol.

This is not lifestyle advice. This is mathematics. Your timeline is fixed; your savings rate is variable.

Until next time,

Want to accelerate your progress?

It’s packed with real-world examples, templates, and prompts to help you transform technology anxiety into a career advantage. Sign up now and take the next step toward building an AI-resilient, financially free future.

Take the uncertainty out of AI and technology change with my Free AI Confidence Guide. It’s built for midlife professionals managing their cash flow, investments, and career pivots:

Turn technology anxiety into strategic career opportunities

Get simple templates, checklists, and real-world examples

Learn practical steps to make AI work for your financial goals