Balance Sheet for Financial Independence: The Non-Negotiable First Step

FINANCIAL INDEPENDENCE

Trixy

7/11/20256 min read

No Shortcuts, No 40-Year Plans: The Midlife Professional’s Accelerated Roadmap

If you’re in midlife and just now starting to think about financial independence, ignore the advice aimed at 25-year-olds. You don’t have decades to wait for compounding to work its magic. You need a no-nonsense, accelerated roadmap: ten years, maximum.

The good news? As a midlife professional, you’re likely already ahead: you’re earning well and have built some wealth.

But there are no shortcuts. The brutal truth: you must deal with the boring, non-negotiable basics. Creating a balance sheet for financial independence is the first step: skip it and you’ll stay stuck.

Why I Ditched the Old Rules

Let me be upfront: I’ve always taken a different path. Everyone around me—family, friends, colleagues—followed the standard script: get a good education, land a stable job, buy a house, settle in for the long haul. I was raised to believe that security came from ticking those boxes. For years, I tried to fit in with that mindset, but something was missing.

I only discovered the concept of “financial independence” seven years ago. Until then, I didn’t even know it was an option. I’m not there yet, but I’ve achieved a lot in these seven years. I’m now on the verge of leaving my 9-to-5 and stepping into real financial independence. The difference? I learned to question the old rules and start with the basics—like building a balance sheet for financial independence and focusing on assets, not liabilities.

The Real First Step: Know Where You Stand

You can’t change your financial future if you don’t know where you stand today. The very first step—no matter your age or background—is to create a balance sheet for financial independence. This isn’t just for accountants or business owners. If you want to take control of your financial future, you need a clear, honest snapshot of your finances.

A balance sheet shows what you own (assets) and what you owe (liabilities) at a specific point in time. It’s the foundation for every decision that follows.

The Jaspreet Singh Principle

Jaspreet Singh, founder of Minority Mindset, sums it up:

“Assets put money in your pocket. Liabilities take money out of your pocket. Know the difference!”

Assets: Anything that increases your wealth or generates income.

Liabilities: Anything that drains your wealth or creates ongoing expenses.

This is the opposite of what most traditional finance advice tells you. The old-school approach—what you’ve heard from mainstream gurus and your parents—usually goes like this:

Buy your own home as soon as possible, even if it means a 30-year mortgage.

Focus on paying off your house and treat it as your biggest asset.

Assume long-term, slow growth is the only way.

Singh’s method is different. Don’t automatically treat your home as an asset: unless it generates income, it’s often a liability due to ongoing costs. Prioritise building a portfolio of assets that actually generate cash flow or appreciate in value. Avoid tying up your money in liabilities that look impressive but drain your finances.

This approach resonated with me. It’s about speed and efficiency: buy assets, not liabilities. Build wealth in a focused, accelerated way: no 30-year waiting games.

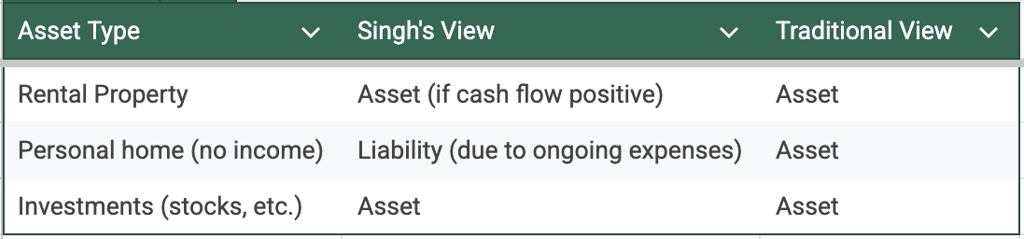

How to Treat Property on Your Balance Sheet: A Contrarian Approach

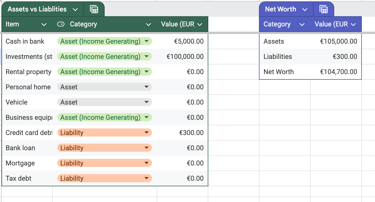

Rental property (cash flow positive): Asset, because it puts money in your pocket.

Personal home (not income-generating): List it under assets for completeness, but be honest: in the Singh framework, it’s not helping your financial independence unless it earns you money.

I don’t fully agree with the idea that a personal home isn’t an asset just because it doesn’t generate income. Even if your home doesn’t produce cash flow, it still has value and can be sold, so it counts as an asset in my view.

That’s why I recommend a balanced approach: combine Jaspreet Singh’s focus on cash flow with the traditional method. We include non-income-generating assets like your home because they add to your net worth. By clearly separating income-generating from non-income-generating assets, you can focus your strategy on what truly drives financial independence, not just what looks good on paper.

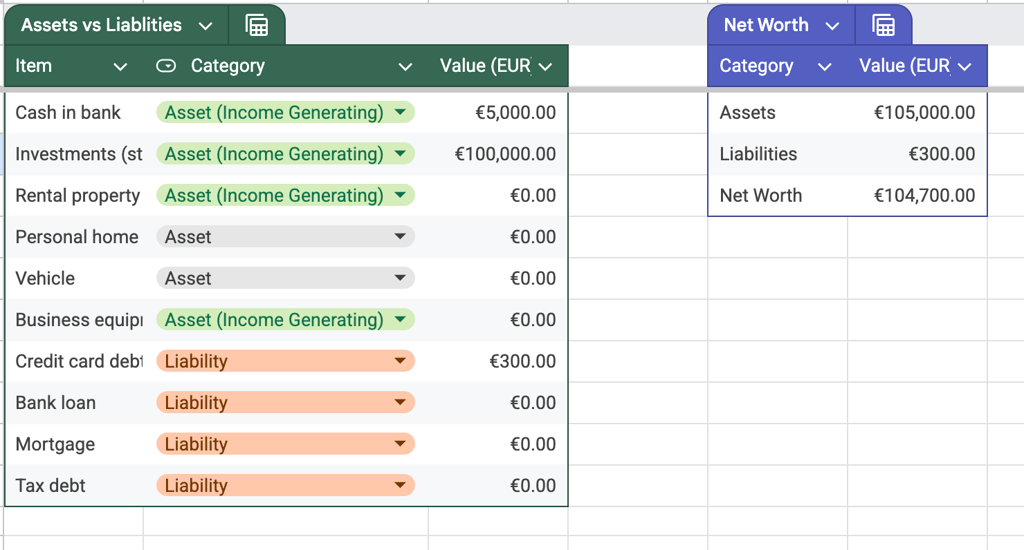

How to Build a Balance Sheet for Financial Independence

Creating a balance sheet for financial independence is about clarity: you need to see everything you own and owe, but also understand which assets actually move you forward.

Step 1: List Your Assets

Break your assets into two categories:

Income-Generating Assets:

These are the real drivers of financial independence: they put money in your pocket regularly.

Rental property (with positive cash flow)

Dividend-paying stocks and funds

Profitable businesses

Business equipment or inventory (if used for income)

Non-Income-Generating Assets:

These have value and can be sold, but do not generate income. They count towards your net worth, but don’t accelerate your progress to financial freedom.

Personal home (unless you rent it out)

Vehicles

Jewellery, art, collectibles

Step 2: List Your Liabilities

Write down all your debts and obligations:

Credit card balances

Loans from banks or other lenders

Mortgage debt

Tax debt

Step 3: Calculate Your Net Worth

Add up your total assets (both types), then subtract your total liabilities. This gives you your net worth.

Formula: Total Assets – Total Liabilities = Net Worth

You can grab my template and get started with your own financial tracking by downloading this Google Sheets document - it's totally free!

What Your Balance Sheet for Financial Independence Tells You

Overall Financial Health

Positive Net Worth:

More assets than liabilities. You’re on the right track. Focus on:

Investing in assets that generate passive income

Increasing your income (promotions, side hustles)

Paying down high-interest debt and redirecting savings

Negative Net Worth:

Owe more than you own. Don’t panic—act:

Make a budget and prioritise debt repayment

Find ways to boost your income

Explore debt consolidation or refinancing

Warning Signs to Watch For

Low Cash Reserves:

If your liquid cash is less than 3–6 months’ expenses, you’re exposed. Build your emergency fund.

Illiquid Assets:

If most of your wealth is tied up in assets that can’t be quickly sold, you may struggle to access cash when you need it. Diversify where possible.

Make Balance Sheet Reviews a Habit

Updating your balance sheet for financial independence is not a one-off task. Make it part of your monthly routine. This helps you:

Spot patterns and trends in your finances

Identify issues early, before they become problems

Make smarter decisions about spending, saving, and investing

Set a recurring reminder. Treat it like a non-negotiable appointment with your future self.

Final Thoughts

There’s no way around it: if you want financial independence, you need to do the groundwork. That means creating and updating your balance sheet for financial independence regularly. It’s not glamorous, but it’s the only way to get a clear, honest view of your financial reality—and to build a future on your own terms.

If you’re starting in midlife, use your head start: focus, accelerate, and make every year count. Ten years. No excuses.

Want to accelerate your progress?

It’s packed with real-world examples, templates, and prompts to help you transform technology anxiety into a career advantage. Sign up now and take the next step toward building an AI-resilient, financially free future.

If you’re ready to move beyond AI anxiety and master practical, actionable AI strategies tailored for professionals over 40, grab my free guide:

Until next time,

Sources & Transparency Note

I strive to research each topic thoroughly and present information as accurately as possible. The sources listed above informed this article, though I recognize that our understanding of complex topics continues to evolve. If you notice any inaccuracies or have additional insights to share, please reach out in the comments below. Your feedback helps improve the quality of information for everyone in our community.

References & Further Reading

Minority Mindset. "Home." Minority Mindset, July 11, 2025.